Mastering Investment Strategies for Diverse Portfolios: A Comprehensive Guide to Growth and Stability

In the dynamic world of finance, the pursuit of wealth accumulation and preservation demands more than just sporadic investments; it requires a well-thought-out, adaptable approach. As markets fluctuate and economic landscapes shift, the discerning investor understands that relying on a single asset class or a handful of securities is akin to navigating a storm in a flimsy boat. This is where the power of diverse portfolios and robust investment strategies comes into play, offering a critical framework for achieving financial objectives with greater resilience.

This comprehensive guide delves into the essential principles and practical applications of building and managing investment strategies for diverse portfolios. We will explore the foundational concept of diversification, dissect the critical role of asset allocation, and unpack effective risk management techniques. Furthermore, we will emphasize the indispensable value of long-term investment planning, providing you with actionable insights to construct a portfolio that not only weathers market turbulence but also steadily progresses towards your financial aspirations. Whether you are a novice investor or looking to refine your existing strategy, understanding these core tenets is paramount to fostering sustainable growth and ensuring stability in your financial journey.

Understanding the Foundation: What Are Diverse Investment Portfolios?

At its core, a diverse investment portfolio is a collection of various assets designed to minimize risk while maximizing potential returns. It moves beyond the simplistic notion of owning multiple stocks to embrace a broader spectrum of investment vehicles, geographies, industries, and asset classes. The objective is to create a portfolio where different components react differently to market conditions, thus cushioning the impact of poor performance from any single investment.

The benefits of diversification are profound. By spreading investments across various categories, you reduce what is known as “idiosyncratic risk” – the risk inherent to a specific company or industry. For instance, if one sector experiences a downturn, other sectors in your portfolio might remain stable or even perform well, balancing out the overall impact. This strategic spread helps to smooth out portfolio volatility, providing a more predictable and less emotionally taxing investment experience.

The Core Principle of Diversification: Don’t Put All Your Eggs in One Basket

This age-old adage perfectly encapsulates the essence of diversification. When you concentrate all your capital into a single investment, you expose yourself to the full magnitude of its specific risks. A sudden negative event affecting that particular company or asset can decimate your entire investment. Conversely, by distributing your capital across a range of assets, you dilute the impact of any single failure.

The key to effective diversification lies in understanding correlation. Assets with low or negative correlation tend to move independently or in opposite directions. For example, during economic downturns, equities might fall, while certain bonds or precious metals might rise, providing a hedge. A truly diverse portfolio strategically combines assets that behave differently under varying market conditions, ensuring that not everything is impacted simultaneously by a single economic shock. This thoughtful integration of various assets is a cornerstone of sound investment strategies.

Pillars of Effective Investment Strategies

Successful investing is not about picking a single “winning” stock, but rather about implementing a robust framework of investment strategies that align with your financial goals and risk tolerance. These strategies guide how you allocate capital, manage risk, and adapt to changing market environments.

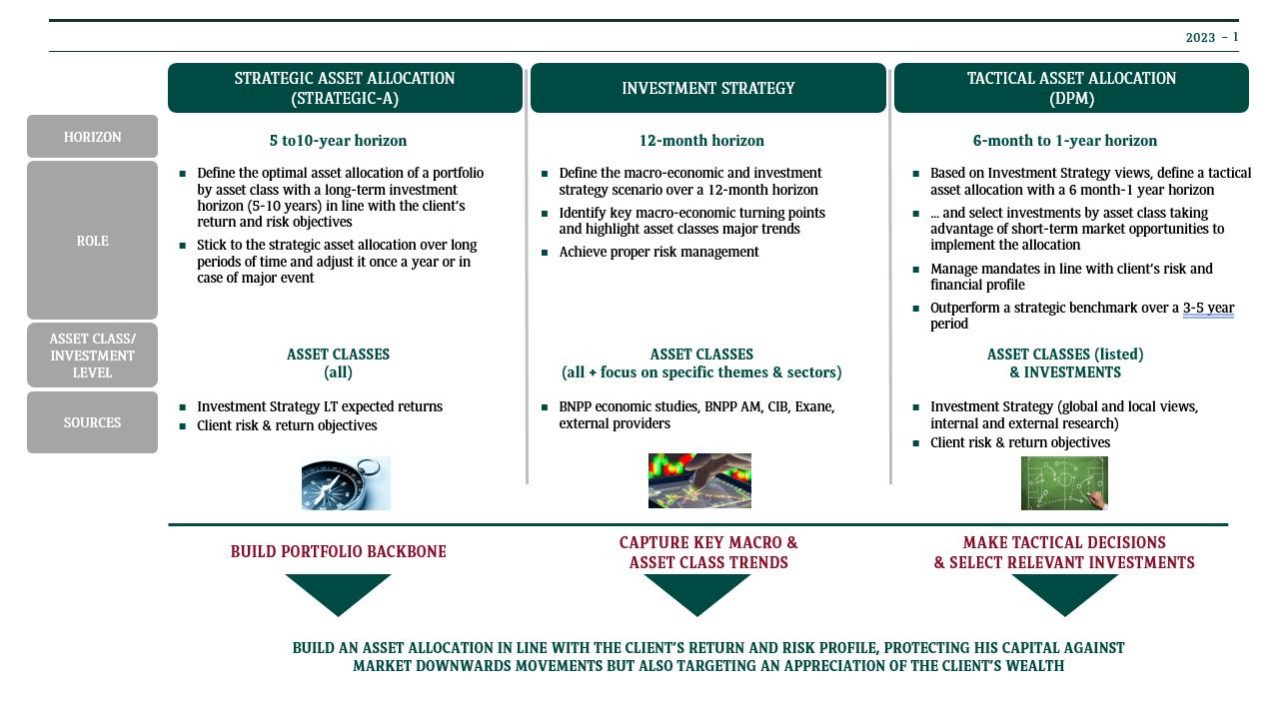

Strategic Asset Allocation: The Cornerstone of Diverse Portfolios

Asset allocation is arguably the most critical decision an investor makes. It refers to the process of dividing your investment capital among different asset classes, such as equities (stocks), fixed income (bonds), real estate, commodities, and alternative investments. The fundamental principle is that different asset classes offer varying risk and return characteristics and often perform differently under various economic conditions.

For example, equities historically offer higher long-term returns but come with greater short-term volatility. Bonds, on the other hand, typically provide lower returns but offer greater stability and income. A common starting point for many investors is the 60/40 portfolio (60% equities, 40% fixed income), which aims for a balance of growth and stability. However, your ideal asset allocation should be highly personalized, influenced by your age, time horizon, financial goals, and most importantly, your risk tolerance. A younger investor with a longer time horizon might opt for a higher equity allocation, while someone nearing retirement might favor a more conservative approach with a greater bond allocation. For a deeper dive into personal risk assessment, consider reading more about understanding your risk tolerance [Internal Link Suggestion: Link to an article titled “Understanding Your Investment Risk Tolerance: A Guide”].

Tactical Asset Allocation: Adapting to Market Conditions

While strategic asset allocation sets the long-term framework, tactical asset allocation involves making short-term, deliberate adjustments to your portfolio’s asset mix. This approach is more active and attempts to capitalize on perceived short-term market opportunities or mitigate immediate risks. For instance, if an investor believes that a particular sector is poised for strong growth in the coming months, they might temporarily overweight their portfolio in that sector.

It’s crucial to distinguish tactical allocation from market timing, which involves trying to predict market tops and bottoms – a notoriously difficult and often unsuccessful endeavor. Tactical allocation is typically a less frequent adjustment, based on a disciplined analysis of economic indicators and market trends, rather than impulsive reactions. While it can potentially enhance returns, it also introduces more complexity and the risk of being wrong, making it generally more suitable for experienced investors or those working with financial advisors.

Core-Satellite Strategy: Balancing Stability and Growth

The core-satellite strategy combines elements of both passive and active investing. The “core” of the portfolio consists of broadly diversified, passively managed investments, such as low-cost index funds or ETFs, representing the majority of the portfolio’s assets. This core provides stable, market-like returns and minimizes management fees. It is built for long-term investment planning and stability.

The “satellite” portion comprises a smaller percentage of the portfolio, invested in actively managed funds, individual stocks, specific sectors, or alternative assets. These satellite holdings are chosen with the aim of outperforming the market or exploiting specific opportunities. This hybrid approach allows investors to benefit from the stability and efficiency of broad market exposure while reserving a portion of their capital for potentially higher-growth, higher-risk ventures. It’s an excellent way to balance the desire for market participation with the pursuit of alpha (returns above the market average).

Dollar-Cost Averaging: Mitigating Volatility

Market volatility can be a significant psychological hurdle for many investors. The fear of investing a large sum right before a market downturn often leads to procrastination. Dollar-cost averaging (DCA) is an investment strategy designed to mitigate this risk. It involves investing a fixed amount of money at regular intervals, regardless of market conditions.

For example, instead of investing $12,000 all at once, you might invest $1,000 every month for a year. When prices are high, your fixed investment buys fewer shares. When prices are low, it buys more shares. Over time, this strategy helps to average out your purchase price, reducing the impact of short-term price fluctuations. DCA takes the emotion out of investing, promotes disciplined savings, and can be particularly effective for long-term investment planning in volatile markets. It ensures consistent participation without the pressure of timing the market perfectly.

Value Investing vs. Growth Investing: Different Paths to Returns

Within the equity component of diverse portfolios, two prominent investment strategies are value investing and growth investing.

- Value Investing: This strategy, famously championed by Benjamin Graham and Warren Buffett, involves identifying and investing in companies whose stocks appear to be trading below their intrinsic value. Value investors look for companies with strong fundamentals, solid balance sheets, and consistent earnings that the market may have overlooked or undervalued due to temporary setbacks or negative sentiment. The belief is that eventually, the market will recognize the true value, leading to appreciation.

- Growth Investing: Conversely, growth investors focus on companies that are expected to grow at an above-average rate compared to the overall market. These companies often reinvest their earnings back into the business, have innovative products or services, and operate in rapidly expanding markets. Growth stocks typically trade at higher price-to-earnings ratios, reflecting their future potential, but also carry higher risk if growth expectations are not met.

- Market Risk (Systematic Risk): The risk that the overall market will decline, affecting most investments. Diversification cannot eliminate market risk.

- Inflation Risk: The risk that inflation will erode the purchasing power of your investment returns over time. Fixed-income investments are particularly susceptible.

- Interest Rate Risk: The risk that changes in interest rates will negatively impact the value of fixed-income investments.

- Liquidity Risk: The risk that you may not be able to sell an investment quickly enough at a fair price.

- Credit Risk: The risk that a bond issuer will default on its payments.

- Currency Risk: For international investments, the risk that changes in exchange rates will reduce your returns.

Both strategies have proven successful, and a well-diversified portfolio can judiciously incorporate elements of both. For instance, a core-satellite approach might use value stocks for the stable core and growth stocks for the more dynamic satellite portion.

Implementing Robust Risk Management for Diverse Portfolios

While diversification is a powerful tool for mitigating specific risks, it is not a guarantee against all losses. Effective risk management encompasses a broader set of practices designed to identify, assess, and control potential threats to your investment capital. It’s about understanding the various types of risks and proactively implementing measures to protect your portfolio.

Identifying and Assessing Investment Risks

A crucial step in risk management is recognizing the different types of risks that can impact your investments:

Understanding how these risks specifically impact different asset classes within your diverse portfolios is essential for crafting appropriate mitigation strategies. For instance, while equities are more exposed to market risk, they can also offer a hedge against inflation in the long run.

Portfolio Rebalancing: Maintaining Your Desired Risk Profile

Over time, the initial asset allocation you meticulously established will drift. Some assets will perform better than others, causing their proportion in your portfolio to grow, while underperforming assets shrink. This drift can inadvertently expose you to more risk than you initially intended. This is where portfolio rebalancing becomes a vital risk management technique.

Rebalancing involves periodically adjusting your portfolio back to its target asset allocation. This usually means selling a portion of your overperforming assets and using the proceeds to buy more of your underperforming assets. This disciplined approach ensures that your portfolio’s risk level remains consistent with your comfort zone and long-term goals. Rebalancing can be done on a time-based schedule (e.g., annually) or a threshold-based schedule (e.g., whenever an asset class deviates by more than 5% from its target). For example, if your target is 60% stocks and 40% bonds